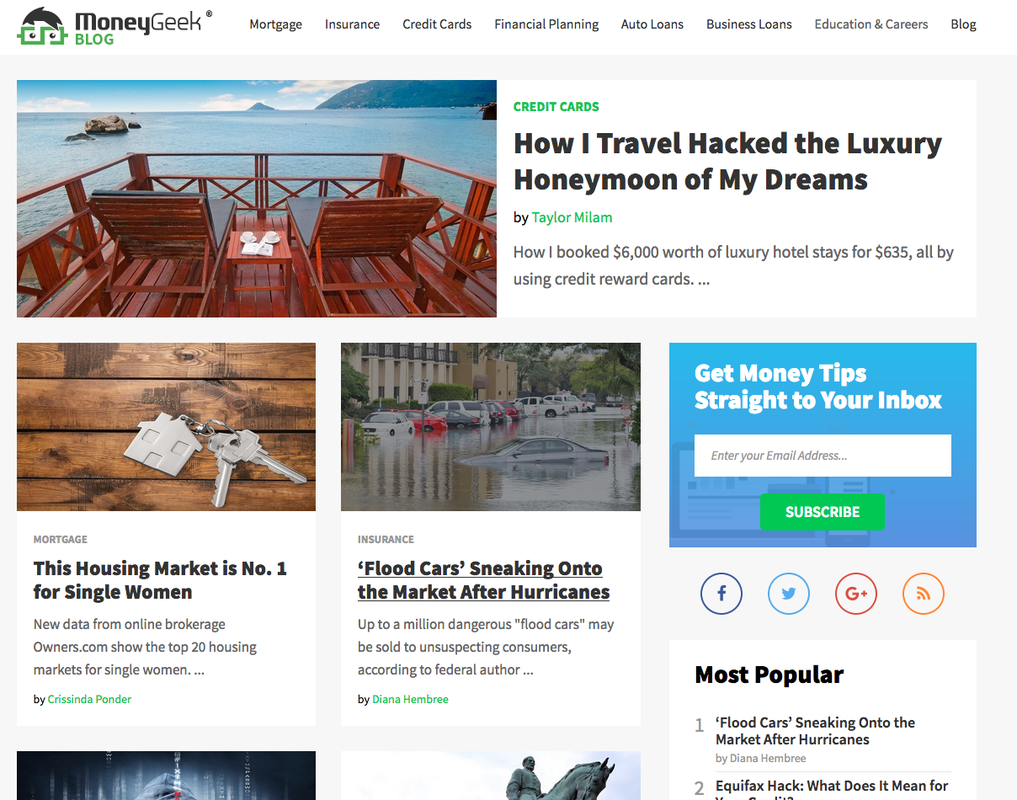

‘Flood Cars’ Sneaking Onto the Market After Hurricanes

Andrew Shawcroft was pleased with the new car he bought from an Oregon dealership in 2015: a 2004 Nissan Murano that he paid for with $12,000 in cash. What the 27-year-old high school teacher didn’t realize was that it had all the signs of a “flood car” – a vehicle transported from the East Coast soon after Hurricane Sandy whose electrical system was so badly damaged a mechanic would later find it was in danger of exploding.

“The car only had about 65,000 miles on it so it seemed like a good deal,” Shawcroft recalls. “During the test drive, it was fine. But during a five-hour trip soon afterward, the cruise control didn’t work and the key fob didn’t either. And two weeks later, it broke down completely.”

Shawcroft, who won an arbitration hearing against the dealership, was one of hundreds of thousands of Americans hoodwinked into buying a flood car after hurricanes Katrina, Sandy, Rita, Andrew, and Hugo. Now, in the aftermath of the massive flooding that accompanied Harvey and Irma, federal officials are warning that a new wave of flood cars are likely coming, and that car buyers had best beware.

“Flood cars are a huge problem,” says Rosemary Shahan of Consumers for Auto Responsibility and Safety (CARS). “There’s no way to make them safe. They’re basically rotting from the inside out and are loaded with bacteria and other contaminants that can cause serious health issues. But they will soon be popping up all over the country, including dealerships that will sell some of them as ‘new’ cars.”

Last week, the Department of Justice issued an advisory warning about auto fraud after hurricanes Harvey and Irma. In a September 14 memo, the agency said that it is anticipating “a high volume of flood-damaged automobiles” to be sold by unscrupulous dealers.

“After past hurricane events, authorities reported truckloads of flooded vehicles being taken out of the impact zone where they were dried out, cleaned and readied for sale to unsuspecting consumers in states that do not brand flood vehicles,” the DOJ reported. “Due to Hurricane Harvey and Hurricane Irma, as many as 1 million flood-damaged automobiles could potentially be passed on to unsuspecting buyers in the coming weeks and months.”

Flood damage from the hurricanes damaged thousands of vehicles, ruining their electrical systems and making airbag sensors prone to failure, the agency warned.

Consumers may buy flood cars labeled as “new” or “certified” — sometimes with factory warranties or extended service contracts — and think they are protected, Shahan said.

“They are in for a rude awakening,” she said. “When problems arise, the manufacturers and extended service companies won’t honor the warranties or service contracts, because the flood damage makes them void.”

In many cases, Shahan says insurers, who should be scrapping the cars, instead arrange for them to be towed away and auctioned off to the highest bidder. That amounts to fraud, she said. “It’s quite clear they will be resold fraudulently.”

How to avoid buying a flood carThe Department of Justice advises consumers to find out about a vehicles’ history before making any purchase decisions.

First, check for visible signs of a flood car – Consumer Reports advises looking for the smell of must or mildew (or a heavy detergent smell from someone trying to disguise it), a visible water line on headlights or tail lights, debris or caked-on mud in the engine or rusty unpainted screws under the dashboard.

Next, look up the car’s Vehicle Identification Number, or VIN – its unique identifier – on the National Motor Vehicle Title Information System (NMVTIS). Run by the Bureau of Justice Assistance, the system is designed to prevent concealment of flood damage and other damage in the vehicles’ history. Car insurance companies are required to report to NMVTIS about vehicles they have written off as total losses.

For a few dollars or less, consumers can use an approved provider such as VinSmart or VinAudit.com to check the DOJ’s system to look up crucial information on the vehicle they’re planning to buy, including its title, recent odometer reading and the history of its “brand” – a label used by states to identify a vehicle’s current or past condition. Consumers can protect themselves by avoiding cars labeled “junk,” “salvage,” or “flood.”

“If the car shows up [as a total loss] on the NMVTIS, you don’t need to look further,” says Shahan.

The NMVTIS database won’t reveal all problems, however. It doesn’t include vehicles with major damage below the threshold of “total loss.” Lesser levels of damage, which can also affect safety, may be revealed on other databases like Carfax Inc., an online commercial service that supplies vehicles’ service and repair history. Then again, Carfax may not reveal whether the car is damaged or even a total loss, unless an insurer has voluntarily reported it.

“Reporting to Carfax is voluntary, so insurance companies don’t have to report the car’s history to it,” says Shahan. “All databases have gaps, so it’s important to get an inspection from a good mechanic, too.”

The Nissan that died in two weeksShawcroft is a case in point. Before he bought his Nissan Murano, he looked up the car’s history on Carfax and had seen nothing to worry about. Then two weeks later, it died on Highway I-5 as he was driving it to Portland for a wedding. Stressed and overwhelmed, he ended up missing the rehearsal dinner.

A mechanic he’d known for a long time inspected the car and told him it had so many problems, he couldn’t even give him an estimate for repairs.

Shawcroft contacted the dealership that sold him the car and the dealer offered to take the car back for $2,000 – a $10,000 loss to Shawcroft. Further investigation showed the car had been bought at auction, had its engine replaced and was full of exposed wires and broken tubing, giving it the potential to explode and catch on fire while in use.

Shawcroft’s case went to arbitration, and he and his attorney, John Gear, prevailed in a hearing.

The dealership had to pay for the car, court fees and attorney’s fees for a total of about $30,000.

Shawcroft feels like he had a narrow escape. Not everyone in his situation is so lucky, he says.

------------------------------

Diana Hembree is senior editorial director of MoneyGeek.com, specializing in insurance issues and a regular contributor to Forbes.com. Co-writer Steve Evans is a regular contributor to MoneyGeek whose work has appeared in Benzinga, Yahoo Finance, MSN Money, and other outlets.

RSS Feed

RSS Feed