State issues grace period order for insurance deadlines

Salem – The Oregon Department of Consumer and Business Services issued a temporary emergency order today in response to the COVID-19 outbreak. It requires all insurance companies to extend grace periods for premium payments, postpone policy cancellations and nonrenewals, and extend deadlines for reporting claims.

The COVID-19 outbreak has caused widespread business closures, job losses, and social distancing measures. This severe disruption to business in the state includes some Oregonians’ ability to make insurance premium payments, report claims, and communicate with their insurance companies.

“During this crisis, we must all do our best to help Oregonians focus on staying healthy, care for their families, and prevent the spread of the coronavirus,” said Andrew Stolfi, insurance commissioner. “Many of our insurers have already stepped up and done the right thing. This order will ensure every Oregonian who needs it has relief from these insurance policy terms, giving them a measure of security and stability.”

Insurance companies must take steps immediately to do the following until the order is no longer in effect:

- Institute a grace period for premium payments on all insurance policies issued in the state

- Suspend all cancellations and nonrenewals for active insurance policies

- Extend all deadlines for consumers to report claims and communicate about claims

- Provide consumers the ability to make premium payments and report claims while maintaining safe social distancing standards

The order is effective immediately, and will be in force through at least April 23. If necessary, the department may extend the duration of this temporary order.

If Oregonians have questions or concerns about their insurance company or agent, they can contact the department’s advocacy team at 888-877-4894 (toll free) or visit dfr.oregon.gov for more information or to file a complaint.

For insurance and financial services information related to COVID-19, visit the department’s website:

https://dfr.oregon.gov/insure/health/understand/Pages/coronavirus.aspx.

|

0 Comments

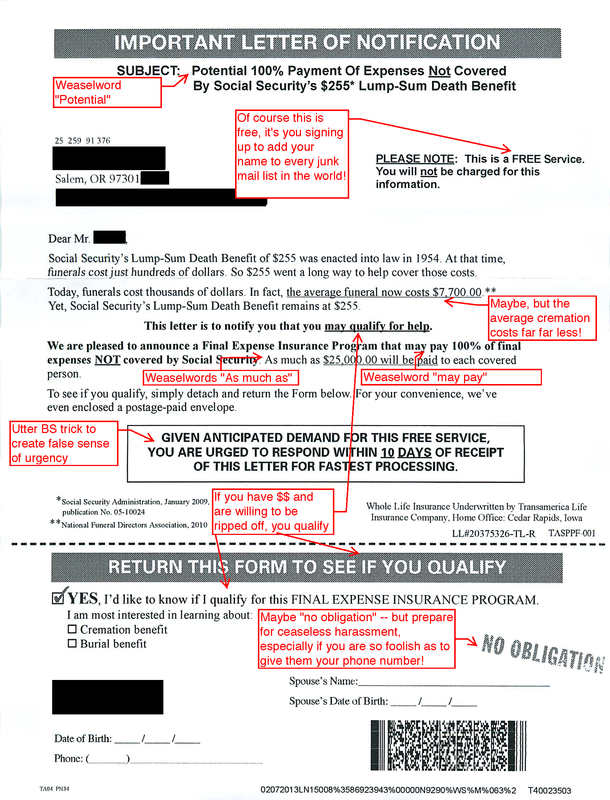

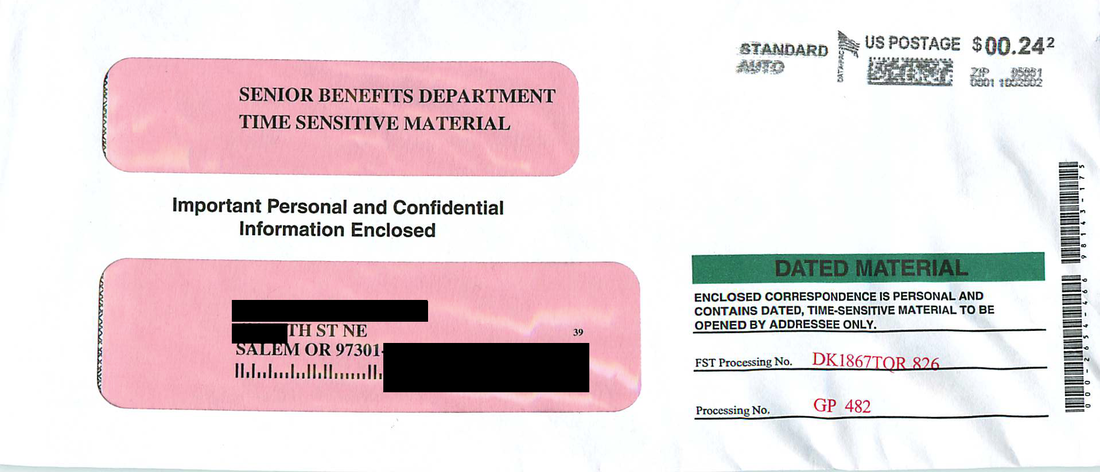

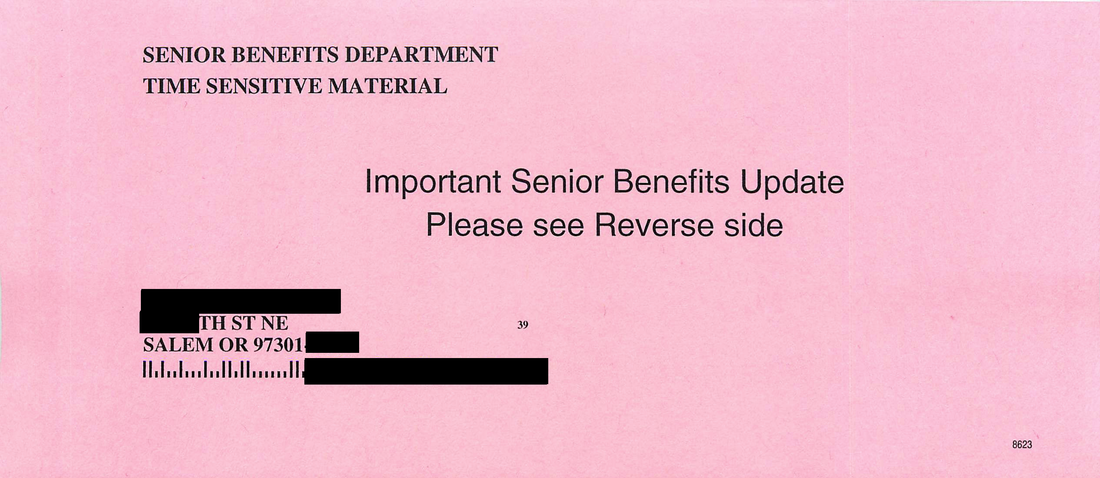

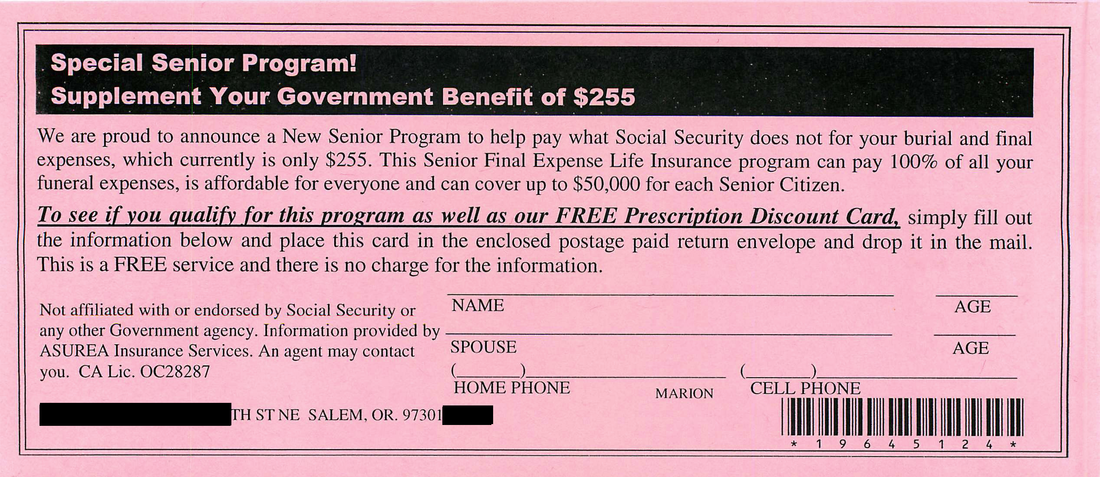

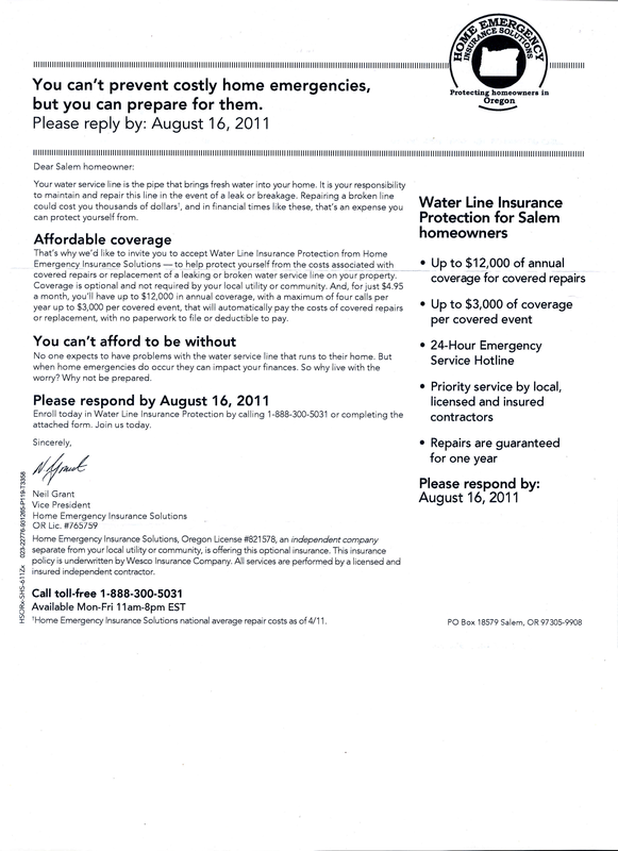

Note the attempts to make it seem to come from a government source The folks who prey on the elderly -- the Elderscammers -- never tire of trying to make their scam letters appear to come from an official source (anything that will get you to open them). When you get mail in an envelope that looks like this, your best bet is probably to recycle it immediately without even opening it.

If you are really torqued about their deceptive technique and want to make it a bit more expensive for them, here's one thing you can do: Open the envelope, but only so that you can find out if there is a postage-prepaid "Business Reply Envelope" inside (there often are). If there is a BRE, take a dark marker and write "STOP SENDING ME JUNK" on the reply card, and draw a big X over the part where they want you to give them all your personal information. Then stuff everything they sent you into the BRE, seal it, and drop it in the mail. This has proven remarkably effective at getting them to stop sending me any such junk. Sadly, all my elderly neighbors and friends keep me well supplied in examples of this kind of scam. (This one was another come-on for funeral expenses insurance, the biggest ripoff this side of waterline insurance plans.)  Mixed in with the many honest businesses, I'm sad to say that there are a TON of ethically challenged businesses out there too. They especially prey on elders, offering them outrageously overpriced goods and services, using all the time-tested tricks of the trade, trying to make it look like they are doing you a favor, and that you might have to "qualify" to do business with them -- when the only qualification is excessive trust in strangers by you, and a willingness to give out private information to total strangers. These people will use any information they can get to take advantage of you (and they will sell and trade that information to similarly exploitation-minded outfits -- along with the key fact, that you were so foolish as to respond to their mailing). There's a good saying that "Good deals don't call you on the telephone" and the same goes in spades for junk mail like this. Honest businesses don't try to make money off you by selling you wildly overpriced insurance. I wish there was a way to require outfits like this to put a skull-and-crossbones watermark on every page of every letter they send out, because then you'd have a chance of realizing what pirates they are.  The last time I called one of these things a scam I got a call from a $500 an hour law firm in Virginia who insisted that I remove the post because, no matter how absolutely horrible, no good, outrageously overpriced, predatory, just-this-side-of-illegally-deceptive and slimy their product was, they felt I disparaged them by calling it a scam. So, lesson learned. This may not be a scam -- the company below may indeed pay claims purchased under this absolutely horrible, no good, outrageously overpriced, predatory, just-this-side-of-illegally-deceptive, slimy insurance offer. But you'd be a fool to find out, because you'd have to buy one to find out, and that would mean that you'd not only pay an absurd amount for a tiny benefit, but you'd also find yourself getting a blizzard of mail from similar outfits, because these outfits all trade "sucker lists" as they refer to them, and once you take the bait on one, they all cast their lines in your direction and try to reel you in. Don't fall prey to these kinds of things. If you're concerned about funeral expenses, contact the Funeral Consumer Alliance of Oregon, an affiliate of the national Funeral Consumers Alliance and learn more about how to minimize the costs for disposing of your remains, and how to avoid getting taken. And remember the basic rule: never do business with anyone who tries this kind of deceptive marketing (the attempt to make their commercial pitch appear to be an official letter). The simplest and best thing to do: just recycle it without even opening it.    New Long-Term Care Insurance Claims Protections

By: Oregon Insurance Division July 10, 2012 -- Oregonians who have long-term care insurance now have the right to have their claims paid promptly and to appeal an insurance company decision to deny benefits. The changes are due to a 2011 law that became effective for people who buy new policies starting July 1, 2012. For those with existing policies, the law is effective when their policy renews, meaning it will be phased in over a year’s period. “Consumers with long-term care insurance policies have not had the same protections as consumers with other health insurance claims, yet they are some of the most vulnerable Oregonians,” Oregon Insurance Commissioner Lou Savage said. “Now, people with long-term care insurance or their representatives can more easily challenge claim denials or delays, which are the most typical complaints we receive,” Savage added. Long-term care insurance covers people who are chronically ill in a variety of settings – at home, in assisted living, or in a nursing home, for example. Typically, people become eligible for benefits if they can no longer perform certain daily activities such as eating, dressing, or bathing or if they have a mental impairment such as dementia. Highlights of the law

Rules establishing long-term care insurance appeals procedures and the requirement that insurers pay claims promptly can be found here: http://insurance.oregon.gov/rules/attachments/recently%20proposed/id03-2012_rule.pdf. I've reposted the below from David Sugerman's blog. As a nuclear engineer and nuclear submarine officer (before I was an attorney), I studied human errors intensively and am very well-acquainted with the research on human error tendencies in pressure-filled situations. The conclusion of that study?

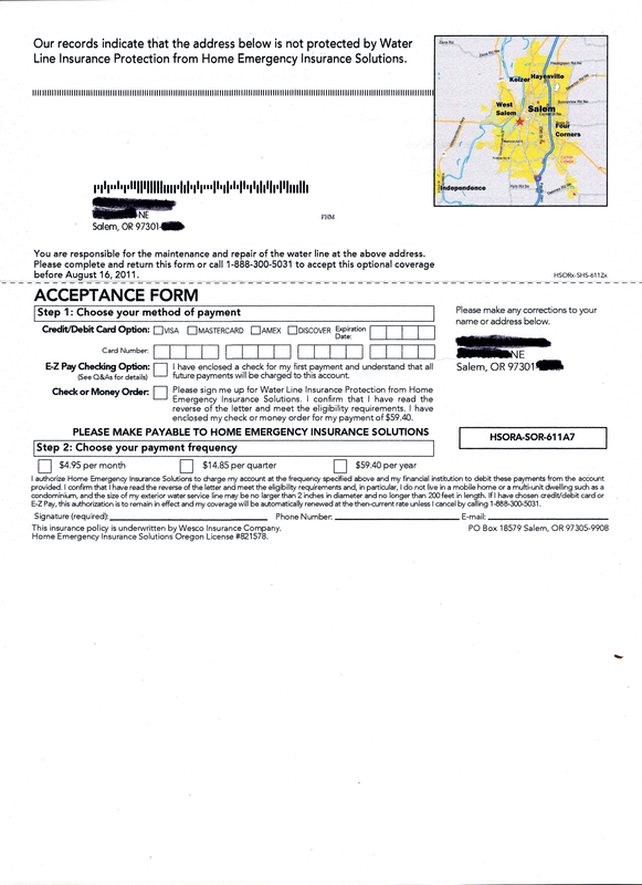

Nearly everything about how modern American medicine is organized is BAD for patient safety and INVITES DANGEROUS ERRORS that hurt people. NASA, the submarine force, the aerospace industry, and computer manufacturing are just a few example of where errors are systematically studied and analyzed and changes made TO PREVENT THE SAME MISTAKES FROM HAPPENING AGAIN AND AGAIN. But hospitals (especially) and medicine as a whole fight tooth and nail to resist all of the best practices designed to eliminate dangerous errors. There is a problem that high malpractice premiums highlight -- but that problem is a "system" that systematically ignores patient safety. Instead of focusing on reducing the harm from errors, they concentrate almost all efforts on preventing the victims of these systemic errors from trying to seek justice. As an attorney who focuses on consumers, elders, and nonprofits, I don't have a dog in this fight - I'm not writing as someone who brings claims over violations of patient safety. But as someone with a lot of training in identifying and managing high-risk operations safely, I know that I'm always floored when I go to hospitals and clinics by how absolutely primitive these places are in their (dis)organization, and how often it's just a matter of luck that even more people aren't hurt by their dealings with the medical system. Here's the original post: Memo to the Oregon Legislature: Healthcare Transformation Starts with Patient Safety The Oregon Legislature is back in session and grappling with proposed health care transformation. Yesterday, we learned that some legislators are more concerned about “defensive medicine” and putting an arbitrary limit on access to justice for Oregonians who are on the Oregon Health Plan or Medicaid rather than they are about keeping patients safe. Did you know that more than 98,000 Americans die every year from medical errors? Here is some context: That number is equivalent to a 747 jet liner crashing every day of the year killing all on board. So when we talk about healthcare transformation, shouldn’t we really be talking about patient safety? We need to focus on the real problem with health care delivery and that is keeping patients safe and informed. Recently, Legacy Emanuel participated in a national study where they implemented simple procedures and check lists for all hospital staff to follow. You know, things like washing your hands between each patient, making certain all medical equipment is accounted for before finishing a surgery, that the patient is the same person as the chart on the end of their bed. According to the Oregonian’s report on that study, Legacy saved over $13 million in one year, cut down on medical errors and significantly lowered their infection and injury rates. Imagine the cost savings if these check lists and procedures were implemented in every Oregon health facility. Imagine the health improvement and lives saved from real health care transformation that starts with patient safety. Instead of focusing on patient safety, we have legislators holding forth about something they call “defensive medicine,” They are using that label as a tool to put arbitrary monetary limits on patients’ rights. Here is a modest proposal: If we’re going to talk about things like this, let’s resolve to get the facts straight. The label “defensive medicine” presumably refers to tests ordered by a provider for purposes of preventing or defending against a lawsuit. A provider who orders testing with no therapeutic value commits insurance fraud, violates Oregon law, and ignores the first rule of medical ethics to do no harm. The doctor who orders unnecessary tests puts the patient at risk by subjecting the patient to an unnecessary medical procedure. And legislators think that Oregon doctors routinely order unnecessary tests, committing Medicare or insurance fraud and putting patients at risk because what? To keep insurance premiums lower? Really? In the same opinion piece there was a second solution to “the problem.” There is a reason for the quotes: No one has ever identified the problem. Even for lack of a problem, some Oregon legislators seek to impose a two-tier justice system. Under the plan that is a solution in search of a problem, the two-tier system would mean two levels of justice. The first tier is reserved for individuals with private insurance. The second tier is for patients on the Oregon Health Plan (OHP). The new legislation would strip OHP patients a basic constitutional right to trial by jury and instead and would limit or cap how much OHP patients can sue for when they are injured due to negligent, substandard medical care. That’s right, under the solution to the non-problem OHP patients claims would be limited even when a provider gives care that is proven to be negligent. The legislators pushing this agenda presumably are doing it in the name of lower doctor malpractice premiums. What they are not saying is that this solution to non-problem has been tried in other states. The result: No noticeable effect on doctor liability insurance premiums. Under this emerging plan, if you have the good fortune to have your own insurance, you would be able to hold a negligent care provider accountable for substandard or negligent care. If a surgeon mistakenly amputates the wrong leg and you are on OHP, the two-tier system of justice would limit your access to justice, no matter how egregious the negligence, no matter how high your lifetime medical costs, no matter your life situation. And this limit would take the form of a fixed limitation set by the Oregon Legislature. Because those who believe that their solution is necessary are also dead certain that the Oregon Legislature is better able to set damages in all cases than a jury that decides each case on the evidence. It’s time that the political agenda of the few take a back seat to patient safety. It is time to make certain that health care transformation puts patient safety first.   My neighbor showed me a letter that she got the other day -- a sales pitch for some of the most overpriced insurance I've ever seen. Oddly, no one in the neighborhood except the seniors got it, and she got it not long after signing up for the property tax deferral allowed for Oregon seniors. My spidey-senses tell me that the scammers keep track of who files for the senior property tax exemption and send them these pitches. I wonder what their response rate is? Whatever it is, it's way too high.

This is a VERY BAD DEAL -- almost pure profit to them, obtained by targeting people who are afraid of unexpected expenses. The basic design -- only the waterline -- and the fine print on this one means that you are very unlikely to ever be able to claim against this policy. Check it out (4 page pdf). Whenever you are approached or sent a mailer selling insurance that only covers a specific risk and that gives you a pitch that plays on your fear of unexpected bills, you should immediately be suspicious. Reputable insurance companies do not sell products like this, particularly with exclusions that gut the coverage. Insurance is too important to let yourself be scammed. If you are in Oregon or especially in the Salem area, I would be happy to review any offers you get like this to help you understand the coverage and the alternatives for managing the risks discussed. |

AuthorJohn Gear Law Office - Categories

All

Archives

December 2022

|

||||

RSS Feed

RSS Feed