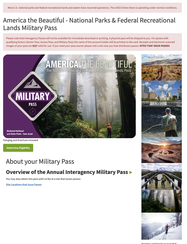

Regular Annual Parks Pass cost $80

Cost for Vets: $10 ($5 processing/$5 delivery)

Get it here: https://store.usgs.gov/MilitaryPass

Cost for Vets: $10 ($5 processing/$5 delivery)

Get it here: https://store.usgs.gov/MilitaryPass

|

Regular Annual Parks Pass cost $80

Cost for Vets: $10 ($5 processing/$5 delivery) Get it here: https://store.usgs.gov/MilitaryPass

0 Comments

If you are a homeowner who has not been making payments on your mortgage and now you are having a problem getting back on track with your mortgage, you may be eligible for help from a new legal aid foreclosure defense project, Oregon Homeowner Legal Assistance (OHLA).

If you are low/moderate income and face any COVID-related financial hardship that threatens your homeownership (defaults, lender refusals to modify your loan, etc.) you should seek if OHLA can help you by calling Oregon Homeowner Legal Assistance: 1-855-503-2598.

A MUST-READ if you are or anticipate being in the market to buy a car anytime soon. And for everyone else, a good article to read anyway -- you never know when someone will smash your car for you by driving inattentively and you will be in the market to buy a car on short notice.

Oregon Consumer Justice (OCJ) is making money available to community-based organizations working to support tenants in accessing rent assistance payments or making applications for rent assistance.

There's more information and a link to the application here: https://lnkd.in/gu7JBAzz Many organizations, community leaders, and individuals are hard at work trying to help prevent evictions, which are traumatic and have far-reaching impact on people's well-being. Spread the word about this resource which might help reach community members who don't know there's help available or don't have the ability to access that help. If you have questions, please direct them to either Janet Byrd at [email protected] or Joseluis Maldonado at [email protected]  The federal Consumer Protection Financial Bureau (CFPB) has a website where you can see if there is rental assistance money available that you can access in order to help you avoid eviction for failure to pay rent.

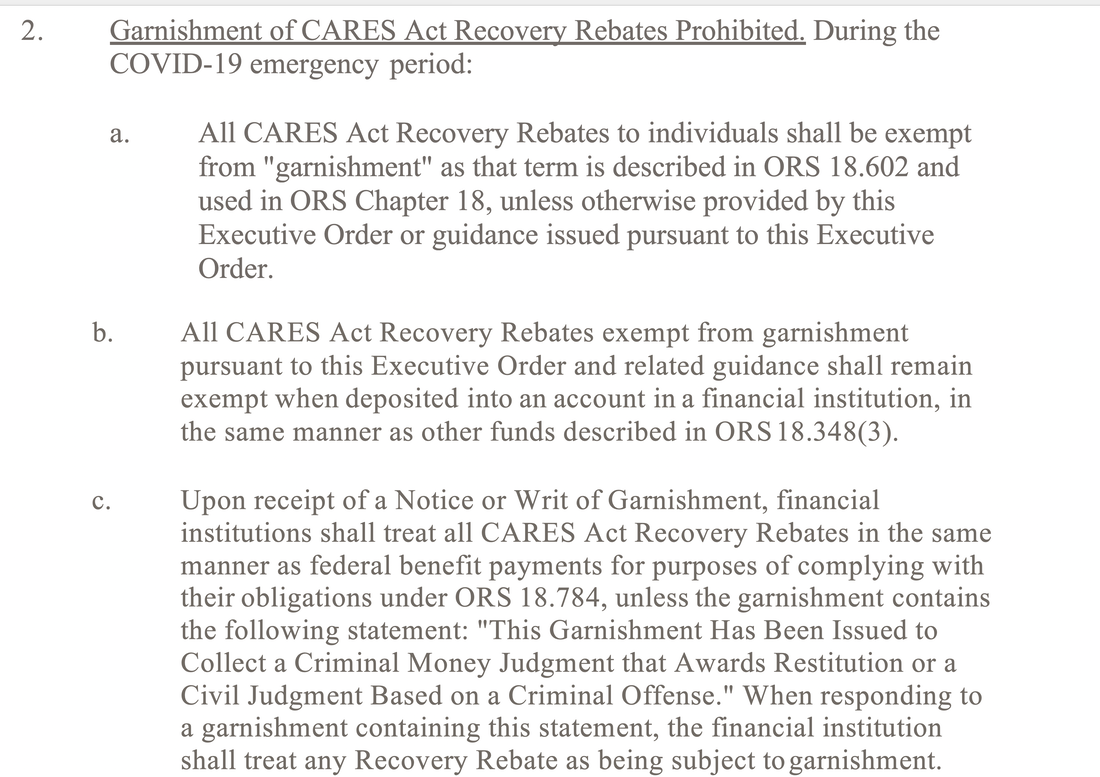

Check it out if you are behind in your rent or utility payments. https://www.consumerfinance.gov/coronavirus/mortgage-and-housing-assistance/renter-protections/find-help-with-rent-and-utilities/ Some elder advocate organizations have put together a pretty good online resource for helping you know how to keep your money safe as you age. (Elders are the main target of scammers.) https://thinkingaheadroadmap.org/money-path/intro Even if you think you have everything all set, it's worth looking these pages over. The Thinking Ahead Roadmap is for everyone, not just people with significant assets. It includes information specifically geared towards "solo agers" (who don't have an immediate family member or partner to step in) and people with complex personal situations. This new tool was designed by Dr. Marti DeLiema of the University of Minnesota and by Naomi Karp and Steve Vernon, research scholars at the Stanford Center on Longevity, with support from AARP and the Society of Actuaries. It's based on extensive research through interviews with experts from multiple disciplines (including elder law attorneys on this list - thanks for your help!), focus groups and an online community forum of over 100 older adults. In addition to the website itself, the roadmap is available in PDF form to download, as are additional helpful documents. In the future, it will be available for ordering in print. Please help spread the word about the Thinking Ahead Roadmap to your colleagues, clients, families and communities.  Oregon has an unclaimed property registry, currently in the Department of State Lands but moving to the State Treasury Office on July 1. You should check it once in a while - it's quick and easy. Just click https://unclaimed.unclaimed.oregon.gov/oregon.gov/ and enter your name.  Coder-turned-Attorney Robb Shector has further enhanced his first big online laws project from his law school days, the excellent online Oregon statutes depository (Oregonlaws.org). Robb has made that even more valuable by coming up with a way to provide a very smooth integration with the statutes from his version of the online Oregon Administrative Rules (OARs). Robb's OARs database now provides hotlinks to statutes so you can easily go check the statutes as you are researching the rules and then easily return to the rules. You can see Robb's administrative rules set here: https://oregon.public.law/rules (photo below of the entry page). Having worked with others (I don't have the technical chops to do the coding myself) to bring readable OARs to Oregonians for a long time (see OregonAdminRules.org tab at top of page), I know Robb put in an awful lot of work. Hats off to Robb for bringing this home at last. It's pathetic that the State of Oregon publishes statutes and rules in such a poorly designed format (all left-justified text that is all but impossible to use without extensive manual reformatting). It would require little or nothing by the state to give Oregonians these important publications in a clear, always-up-to-date, easy to use form, as Robb has shown.   Links to http://www.consumer.law/ The Governor has wisely ordered that any Oregonian's CARES check be free from garnishments by creditors (except for restitution garnishments for criminal justice debts) during the COVID-19 emergency. The top picture is the key provision. If you want the full text and all the details and definitions, the full order is shown below that and you can download it by clicking on the down-facing arrow. Kudos to Gov. Brown for acting to help Oregon families survive this crisis in this critical period.   The heroes at the National Consumer Law Center (NCLC.org) have made their comprehensive 50th Anniversary guide for debtors called “Surviving Debt” available at no charge for ANYONE. This is an outstanding resource for ordinary folks who don’t want to try to read law books or statutes etc. It’s in clear, plain English. I have given away more than two dozen copies to friends and clients and it’s usually the first book I reach for when someone has a question about how to manage their debts of ANY kind. While you isolate in place, if you are worried at all about your finances, take the time to read the first 10 short chapters and then the chapters for your type of debts. So you don't have to read it all -- just the first couple chapters and then the chapters that pertain to your type of problem. (And if you yourself are able to make a contribution to NCLC, they would welcome it and put it to good use.) Find it here: https://library.nclc.org/SD

State issues grace period order for insurance deadlines Fellow consumer attorney Ian Lyngklip of Michigan produced this helpful video that you should watch if you are stressed about bills during work interruption from COVID-19.  Image of Cover of "Collection Actions: Defending Consumers and Their Assets" Fourth Edition by NCLC (National Consumer Law Center) Image of Cover of "Collection Actions: Defending Consumers and Their Assets" Fourth Edition by NCLC (National Consumer Law Center) Guide to Reducing Hospital Bills for Lower-Income Patients by Andrea Bopp Stark As described below, hospital debt poses a significant problem for millions of Americans. This article provides a nine step approach for lower-income patients seeking to eliminate or reduce hospital debt. Medical Debt Is a Widespread and Serious Problem More than 27 million Americans lack any health insurance—58% of low-income working adults, 44% of young adults, and 35% of Latinx adults. In addition, almost 50% of nonelderly adults have insurance that requires high deductibles and significant out-of-pocket costs. In recent years the number of Americans uninsured or underinsured has been growing. As a result, a high number of families are burdened with medical debt:

As a result, there is an urgent need to address consumers’ medical debt problems. A detailed discussion is found in NCLC’s Collection Actions Chapter 9. This article provides a nine step approach for lower-income Americans to reduce or avoid their hospital bills. Step 1: Don’t Prematurely Pay Even Part of the Hospital BillDepending on the state and the patient’s income, the bill may be waived in whole or significantly reduced—there is no benefit in making payments that may not be owed. Nor is there any downside in delaying payment:

Step 2: Determine If the Consumer Is Medicaid EligibleDetermine if the patient is Medicaid eligible. In some but not all states Medicaid coverage is retroactive to hospital bills incurred over the prior three months. Even where a state does not allow retroactive coverage, if the patient is found to be Medicaid eligible then at least for future bills they will have that source of payment for any follow-up treatment or other conditions. Apply for Medicaid by going to www.healthcare.gov or calling 800-318-2596, or at the local public assistance office. Eligibility for Medicaid varies from state to state and depends on family income and may also depend on family resources. Some states limit Medicaid to certain groups of people, such as children and pregnant women. However, people in many states automatically qualify so long as their income is 138% of the poverty line or below. (In 2020 the income limits are: $17,236 for a family of one; $23,336 for a family of two; $29,435 for a family of three; and $6,100 for each additional family member. The poverty line is higher in Alaska and Hawaii.) Sometimes children are eligible for Medicaid even if their parent is not. Medicaid’s Early and Periodic Screening, Diagnostic, and Treatment (EPSDT) requirements mandate coverage of a broad array of diagnostic, preventive, and treatment services for beneficiaries under age 21. In addition to Medicaid, some states may offer other programs to help lower-income patients with healthcare bills. Ask the hospital financial counselor or patient advocacy organizations in your state for more information. Step 3: Determine If a Hospital Is a NonprofitAs described below, a consumer has additional federal rights concerning a hospital bill if the hospital is a nonprofit 501(c)(3) entity, and additional state law rights may apply as well in a few states. To determine if a hospital is a nonprofit, go to the IRS website. In particular, go to the IRS tax exempt organization search page and search by organization name (under the drop down starting with employment identification number). The website will only identify if a hospital is a 501(c)(3) entity. If the hospital is not found, it may be that it is still nonprofit but under a different name (such as hospital’s parent entity) or the name has not been included in this database. It is always wise to check to see if a hospital is a nonprofit even if it does not show up on the above website. Alternative methods of determining if a hospital is nonprofit include checking the hospital’s website, asking a hospital administrator, or talking to the hospital’s billing office. Step 4: If the Hospital Is a Nonprofit, Understand Consumer Rights Under Federal LawThe Affordable Care Act (ACA) (also known as Obamacare) imposes certain requirements on nonprofit hospitals with 501(c)(3) IRS tax status concerning their financial assistance policies for low-income patients. Hospitals must create a written financial assistance policy (FAP) and a written emergency medical care policy. The financial assistance policy must disclose:

Step 5: Whether the Hospital Is Nonprofit or For-Profit, Understand Rights Under State LawUnlike federal law, state laws often specify standards for how much financial assistance a hospital must provide a patient of a given income level, and these state laws typically apply both to for-profit and nonprofit hospitals. But applicable state law varies significantly from state to state. For example, ten states have enacted laws that require hospitals to provide a full spectrum of free and discount care for patients under specific eligibility standards, primarily based on income: California, Connecticut, Illinois, Maine, New Jersey, New York, Nevada, Rhode Island, Washington, and Maryland. On the other hand, five states (Hawaii, Montana, New Hampshire, Wisconsin, and Wyoming) have no financial assistance requirements. The other thirty-five states are somewhere in between. Even among the ten states that have strong protections, there are differences. In Maine, all hospitals must provide free care for patients whose household income is up to 150% of the federal poverty level (FPL), but there is no discount care at all for those with higher incomes. Illinois on the other hand requires all hospitals to provide free care for those who are uninsured with family income of up to 200% of the FPL or up to 125% FPL for rural or critical access hospitals. But Illinois also mandates discount care for those with family income of up to 600% of FPL. A number of states provide requirements only for nonprofit or state hospitals (Oregon, Texas, and Louisiana). Some states provide assistance directly from the state for hospital bills (Massachusetts, Colorado, and South Carolina). There are even more variations in other states. Detailed state-by-state summaries of financial assistance requirements are available from two NCLC resources: NCLC’s An Ounce of Prevention: A Review of Hospital Financial Assistance Policies in the States (Jan. 2020) and NCLC’s Collection Actions § 9.4.3. An Ounce of Prevention includes eight appendices summarizing each jurisdiction’s type of financial assistance as well as who is eligible, the source of funding for the plans, and the statutes (if any) that mandate the assistance, which allows advocates and legislators to compare their state with the policies in other states. NCLC’s Model Medical Debt Protection Act (Sept. 2019) provides language for a model state law mandating financial assistance for lower-income hospital patients. The model act specifies eligibility guidelines for financial assistance, provides specific guidelines for charity and discounted care, and includes procedural safeguards to protect consumers from aggressive or unfair debt collection practices. A growing number of states have also enacted “surprise” medical debt legislation—at present about half the states have this legislation. Surprise medical debt laws limit bills from out-of-network physicians providing services at an in-network hospital. These laws address the situation in which a patient assumes their insurance covers care at an in-network hospital only to be surprised that an individual doctor’s bill at the hospital is not covered by insurance. There are also some state laws dealing with balance billing—where a hospital agrees to receive less than the full chargemaster price from the insurance company and then bills the patient for the difference. See NCLC’s Collection Actions § 9.4.3.1. Step 6: Obtain the Hospital's Financial Assistance PolicyIt should not be difficult to obtain a hospital’s financial assistance policy (FAP). For nonprofit hospitals, federal law requires hospitals to:

The above requirements apply to nonprofit hospitals, but for-profit hospitals may use some of the same methods to publicize their policies. If all else fails, ask the billing office for a copy of any financial assistance policy. Step 7: Compare the Financial Assistance Policy with State Requirements and the Individual Patient’s CircumstancesMany hospitals will have a financial assistance policy. Federal law requires every nonprofit hospital to have one, some states require all hospitals to have one, and even where a for-profit hospital is not required to have one by federal or state law, it may still voluntarily have such a policy. For example, Vermont hospitals have all voluntarily created financial assistance plans. Compare the policy with any state requirements. In a shockingly large number of cases hospital financial assistance policies do not comply with state law. See NCLC’s Collection Actions § 9.4.3.1. Then compare the policy with the patient’s income and the type of care the patient received to see if the patient qualifies for assistance. Step 8: Applying for Financial Assistance After determining whether the patient’s income and family size qualify under the financial assistance policy, make sure that the hospital procedure is covered by the financial assistance policy. Some procedures such as cosmetic surgery may not be covered. Next, find out how to apply for the assistance. The patient may have to provide a detailed budget, list of assets, information about family members, tax returns, or proof of income. Federal law requires nonprofit hospitals to explain in their financial assistance plan the procedure for applying for financial assistance. If the financial assistance plan does not fully explain the application process, call the hospital’s billing office for more information. Do not delay as many programs only give you about 240 days after the care or procedure to apply for assistance. Federal law places certain requirements on a nonprofit hospital’s handling of an application for financial assistance, such as a denial cannot take place because of missing information not specified in the hospitals disclosure of application requirements. If a nonprofit hospital provides limited financial assistance without even reviewing an application for assistance, the patient still has the right to seek additional assistance. See generally NCLC’s Collection Actions § 9.3.1.5.5. Step 9: If an Application for Financial Assistance Is DeniedIf a patient is denied assistance, some hospitals may have an appeals process. Pay attention to the time allowed for any appeal. There may be steps to preserve a claim for financial assistance. If the patient ultimately does not qualify for assistance, some hospitals provide payment plans to pay off the debt over an extended period of time. But a patient should never agree to a payment plan that the patient cannot afford or that would prevent payment of other of the patient’s debts. Hospital debt should be treated as a lower priority debt compared with rent, utility, mortgage and automobile loans, and most other forms of debt. Non-payment of that other debt will have serious immediate adverse consequences, while hospital debt may have little negative effect for six months (as described above) and it may be years, if ever, before a judgment is taken against the consumer for the debt. Also, hospital debt is unsecured debt that is fully dischargeable in bankruptcy. When a judgment is taken against a patient, it will be important to determine the patient’s exposure to wage garnishment and seizure of bank accounts or other property. But some low-income patients may be totally judgment proof. Be aware that under state necessaries statutes or common law doctrines a spouse may be liable for the other spouse’s treatment and a parent for children’s treatment. For more detail, see NCLC’s Collection Actions § 9.6.  Worthwhile information in here -- worth checking out.

Click on photo above or point your browser to https://www.oregonfuneral.org/  Graphic of website search engine for veterans benefits Click on the photo above to be taken to a cool search engine that compiles state-specific and federal benefits in one place for any state. Here's today's printout for Oregon (subject to updates of course):

The Braille and Talking Book Program

offers Veterans who have difficulty with regular print materials the return of the gift of reading. The Joy and Freedom of Reading Whether escaping into a great novel or staying current with popular magazines, the freedom and independence of reading are only a few steps away. This program, from the National Library Service (NLS) and the Library of Congress, provides talking books, audio magazines, and digital talking-book players free of charge. Any honorably discharged Veteran who is * blind * has low vision, or * a disability preventing the reading of traditional materials is eligible. Participants choose whether their selected reading materials are delivered by mail, downloaded from the web-based service BARD (Braille and Audio Reading Download) or through the BARD mobile app for smartphones and tablets. NLS maintains a vast catalog of titles and publications from the latest best-sellers to timeless classics. Plus, Veterans have preferential status in the lending of materials and equipment. The Braille and Talking Books Program is accomplished through a nationwide network of libraries to serve citizens and Veterans living inside the U.S. or abroad. Applying for this service is easy. Call the National Library Service at 1-888-NLS-READ (1-888-657-7323) or visit them on the web at www.loc.gov/ThatAllMayRead Veterans served to protect freedom. Now let National Library Service provide the freedom for all to read.  Where's my VIN?Look on the lower left of your car's windshield for your 17-character Vehicle Identification Number. Your VIN is also located on your car's registration card, and it may be shown on your insurance card.

What this VIN search tool covers

About Us Bankruptcy Exemption Limits (what you can keep) Amounts Going Up  Welcome to Consumers Rising Join the Campaign. Make a Difference. For years, consumers have been under attack from all angles -- financial fraud and deceit, invasions of privacy, roadblocks to our day in court. From predatory lenders to crooked banks and debt collectors, it seems like bad corporate actors are always looking for ways to rip us off and get away with it. That's why our work begins today. Your voice and your experiences are the most powerful tool we have to help change things for the better. CLICK to Join Consumers Rising and get ready to take back control. Your Finger on the Pulse of the Biggest Consumer Stories Do you want to pitch in to hold corporate wrongdoers accountable? Keep up with the latest in consumer protection and how it can impact you. Get the scoop from us and find out how you can protect yourself from predatory business practices and stand up for your rights. First Steps

We are launching a new “Tell YOUR Story” tool that will enable residents, families, ombudsmen, and those who work with them tell their story about nursing home or assisted living care.  John Gear/John Gear Law Office has been a proud Salem Harvest sponsor since it began |

AuthorJohn Gear Law Office - Categories

All

Archives

December 2022

|

|

Lawyerly Fine Print:

John Gear Law Office LLC and Salem Consumer Law. John Gear Law Office is in Suite 208B of the Security Building in downtown Salem at 161 High St. SE. That is right across High Street from the Elsinore Theater, a half-block south of Marion County Courthouse.

John Gear is only licensed to practice law in Oregon. This site may be considered advertising under Oregon State Bar rules. There is no legal advice on this site so do not take anything you read here as advice for your particular problem or situation. And I do not represent you and I am not your attorney unless you have hired me with a representation agreement. While I do want you to consider me when you seek an attorney, you should not hire any attorney based on brochures, websites, advertising, or other promotional materials. All original content on this site is Copyright John Gear, 2010-2022. |

RSS Feed

RSS Feed