Worthwhile information in here -- worth checking out.

Click on photo above or point your browser to https://www.oregonfuneral.org/

Click on photo above or point your browser to https://www.oregonfuneral.org/

|

Worthwhile information in here -- worth checking out.

Click on photo above or point your browser to https://www.oregonfuneral.org/

0 Comments

Graphic of website search engine for veterans benefits Click on the photo above to be taken to a cool search engine that compiles state-specific and federal benefits in one place for any state. Here's today's printout for Oregon (subject to updates of course):

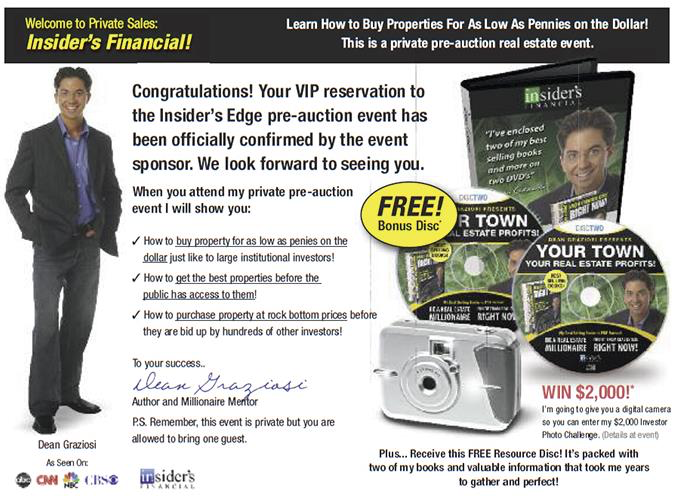

I've had to help several people clients get money back from shady "training" companies that supposedly offer to teach you how to flip real estate for big profits. These slimy people are truly the snake-oil salespeople of the 21st Century. Whether they call themselves "[big name] University" or some sort "seminar" offering "inside information," the only thing you really need to know is this: The only easy money made in real estate is made off people who think there's easy money to be made in real estate. Don't be one of them.  Graphic of slick promotional piece trying to lure people to a "real estate flipping" course A mailer sent by defendants enticing consumers to attend a Nudge “preview event. A Treat Beginning on Halloween for military/Natl. Guard: Free electronic credit monitoring10/31/2019 October 31, 2019 The wonderful Ronni Bennett put a great "intro to Medicare" guide on her blog "Time Goes By." Very helpful. Annual Medicare Enrollment Period has Arrived by Bridget Small  Forced arbitration is a rigged system designed by corporations in which injured workers and consumers have no meaningful chance of finding justice. Forced arbitration requires Americans to “agree” to surrender fundamental constitutional rights – often without ever realizing they’ve done so. When corporations harm workers and consumers by cheating, stealing, or even breaking the law, cases that should be heard by a judge or jury are instead funneled into a secret system controlled by the wrongdoers in which there is no right to go to court, no right to a jury, no right to a written record, no right to discovery, no transparency, no legal precedents to follow, no opportunity for group actions when it would be too difficult or costly to file a claim alone, no guarantee of an adjudicator with legal expertise, no transparency, and no meaningful judicial review. Without such checks and balances, the deck is stacked heavily against workers, patients, and consumers, and systemic misconduct is allowed to continue in secret. Forced arbitration’s proponents counter that the process is faster, fairer, and better for workers and consumers than going to court. However, this comprehensive analysis of the self-reported data provided by the arbitration organizations makes clear that forced arbitration is not an alternative judicial process, but instead eliminates claims, immunizes corporations, and allows abuse, discrimination, fraud, and essentially all other corporate wrongdoing to go unchecked. Americans are more likely to be struck by lightning than they are to win a monetary award in forced arbitration. Click on the image to get a copy of the full report or download it here.

How Collectors Trick Consumers into Reviving Dead Debts Source: The Washington Post Debt collectors are not allowed to sue on old debts that have expired. These debts are so old that there is often little or no proof showing who owes the debt and how much is owed. The most common complaint about debt collectors is that they harass consumers for debts that the consumers do not owe. And debt collectors are finding new ways to exploit loopholes and trick consumers into reviving zombie debts. Oklahoma social worker and mother of five Terrie Raymer was one victim of the collections industry's new tricks. A debt collector garnished 19 cents from Raymer's paycheck and later sued her, claiming that the 19 cent garnishment had brought the debt back to life. Another collector fooled consumers with zombie debts by offering them new credit cards, but then enrolling them into a repayment program for their old debts without their permission. The Consumer Financial Protection Bureau has proposed a new rule that would loosen the standards for debt collectors who sue on old debts by allowing them to argue they did not know the debt was expired. Read More. YOU can help stop zombie debt collection

The Consumer Financial Protection Bureau has extended the comment period for its (terrible) proposed rule on debt collection to September 18, 2019. You can submit your comment through NACA's convenient portal to tell the CFPB that consumers need better protection from unfair zombie debt collection. NACA is also collecting signatures on a petition that will be submitted to the CFPB. Sign and share the petition so we can show the CFPB that consumers want better protection from abusive debt collection tactics. If there was ever a case that showed exactly how forced arbitration encourages and promotes corporate misconduct and arrogance, this is it. A pastor wrongly accused of theft because of Wells Fargo's screwup simply asks for an explanation and for Wells to pay his legal fees, fees he was forced to incur solely because of Wells and its screwup. Wells tells him to go fly a kite, "apologizing" but refusing to cover his legal bills. And now Wells is trying to hide the case behind the stone wall of forced arbitration, where the judge of the case (the private arbitrator) is literally on Wells Fargo's payroll. Starting in the 1970s, a series of radical decisions by the US Supreme Court tossed out the 70 years of precedent barring forced arbitration in employment and consumer cases. Since then, we've seen the entire civil justice system in America has essentially been gutted by these forced arbitration clauses in consumer and employment cases. Corporations use these clauses to cover up when they lie, cheat and steal, and arbitration protects outrageous criminal conduct by corporations by keeping others harmed in the same ways of having any ability to even know that others are fighting the same fight. Forced arbitration is the end of any concept of Equal Justice Under Law in America, and its use is a huge part of the reason that while most Americans are struggling to keep up, the richest of the rich are becoming even richer without bounds.

The Oregon Insurance Commissioner's office sent this around. I say whether you meet with an insurance agent or not is up to you, but having a reasonably accurate home inventory in this day of cell phones is really, really easy and quite worthwhile. Just go through your house, take photos of every room from every angle with cupboards and drawers open. And when you have any particularly valuable item, take several pictures of the item that shows its condition, and also take a picture of the purchase receipt or appraisal. Turn the date/time stamp on with your phone so that it's recorded on each photo. Back up all these photos up to the cloud and to a thumb drive kept in your safe deposit box or at a friend's house (or in a fire safe). Why should you do this? Because the insurance company will turn on you like a rabid dog when you suffer a significant loss -- you're no longer their valued policyholder at that point, you're a suspected thief whose word is absolutely not to be trusted (that's how they see it). Normal people who haven't suffered a big loss are shocked when they find that their formerly oh-so-friendly insurance company (who has been happily taking their premiums all these years) turns sociopathic and paranoid and accuses them of inflating the losses and starts demanding documentation and proof of ownership for every item in the home. Insurers hire battalions of adjusters and train them on how to settle claims for less than they're worth. Worse, the insurance companies are so rich and powerful that they make banks look like sandlot ballplayers, and most people who have not experienced the ordeal of trying to get fair treatment from an insurance company after a total loss are devastated by the second disaster (the first one is the fire or flooding, the second one is the way the insurers treat insureds if those insureds cannot prove every detail of every bit of every claim). Essentially, the insurance companies win by shorting policyholders on damage payments, and the whole time while they do it, they are constantly issuing reminders that it's a crime to commit insurance fraud. Meanwhile, they are all-but unregulated, as they bought themselves immunity from the Oregon Unlawful Trade Practices Act, the statute that lets consumers hold businesses responsible for misconduct in the marketplace. So their conduct isn't even illegal -- it's just what they do. It's kind of like the situation with campaign finances -- the scandal isn't what's done that's illegal, the scandal is what they do that's perfectly legal. And that you have no very little recourse. The only solution I know of is to hire a lawyer so that you do not have to deal with an insurance company yourself if you have any kind of serious loss -- it's like being fed into a meat grinder if you don't have someone to advocate for you and make the insurance company do what it's supposed to under the contract and the the laws. I'm not trying to drum up business here, I don't do that kind of work. But that's the advice I would give any family member in any state who suffers a substantial loss. In other words, the best way to prevent disputes with your insurance company after a loss is to first call a good lawyer who is experienced in insurance claims disputes before you call your insurance company.

What is the Military Lending Act and what are my rights? The Military Lending Act (MLA) is a Federal law that provides special protections for active duty servicemembers like capping interest rates on many loan products. What are my rights under the MLA? Answer: The MLA applies to active duty servicemembers (including those on active Guard or active Reserve duty), spouses, and certain dependents. It limits the interest rates that may be charged on many types of consumer loans to no more than 36% and provides other important protections. (continued) ... Go to the CFPB website for the full Military Lending Act flyer Or click below to download the flyer so you can share it with others.

REMEMBER: Federal law prevents businesses from sticking fine print into their contracts that prohibits you from writing or posting a negative review of the business! (The Consumer Review Fairness Act (“CRFA”) became law in March 2017.)

The Federal Trade Commission recently slapped three companies who had form contracts that said the consumers could not post negative reviews about the products or services from the businesses. Worse, these form contract also had confidentiality clauses -- those said that the consumers would PAY money damages to the businesses if the consumers disclosed information they got while using the products or services was confidential. Good Washington Post Article on How Car Dealers Rip You Off with Financing

Ian Ayres is the William K. Townsend professor at Yale Law School. As websites such as Cars.com and TrueCar have made car pricing more transparent, auto dealers have turned to boosting their profits with hidden fees on loans. When a consumer chooses in-house financing with an auto dealer, the dealer sends the customer’s financial information to a lender and is told the rate that the customer qualifies for. But it’s legal for the dealer to turn around and charge the customer a higher interest rate. You might qualify for a 5.9 percent interest rate, but if the dealer can get you to agree to a loan at 11 percent, the lender will kick back more than $1,000 to the dealership as pure profit. This discretionary markup of the interest rate allows auto dealers to arbitrarily increase their fees. An analysis by the independent online auto-loan marketplace Outside Financial has found that dealers are charging an average markup of $1,791 per loan. By contrast, in 2003, Vanderbilt University economist Mark Cohen estimated that 10 percent of loans to Nissan’s borrowers were marked up more than $1,600. Now the average loan is boosted more than that. . . . Economists have had evidence for decades that car dealers tend to charge minorities higher prices. A series of studies I authored and co-authored in the 1990s found that auto dealers consistently charge black consumers prices that are hundreds or thousands of dollars more than their offers to white shoppers. These inflated prices can more than double the dealer’s profits compared with selling the same vehicle to a similar white customer. . . . The CFPB and other government agencies should be on the lookout for ways to better curtail dealership lending abuses. Yet instead of stepping up enforcement and protecting customers, the CFPB has rolled back rules on discriminatory lending practices and decreased enforcement of existing protections. Just last year, the Senate used the Congressional Review Act to overturn a CFPB rule that explicitly banned auto lenders from charging discriminatory fees on the basis of race. . . . Groups like the US Chamber of Commerce spend extraordinary sums of money on hired hack "scholars" whose mission is to produce propaganda that paints class action lawsuits in a bad light. Their goal is to destroy the class action form of lawsuit, so that their corporate backers can rip people off by the thousands and tens of thousands and not have to pay a price for it. A recently concluded (after 8 years) huge Oregon class action shows the truth, which is 180 out from the Chamber propaganda. The truth is this:

July 16, 2019 In Blog  Reuters has a must-read story with implications for everyone in America:

"That evidence was clearly compelling: In a 2004 ruling, Judge Stephens rejected Purdue’s motion that he dismiss the case and sided with the state’s assertion that the material could convince a jury that Purdue’s sales pitch was full of dangerous lies. But Stephens sealed the evidence on which he relied in that ruling. And when Purdue and the state reached a settlement that year, before the case went to trial, the evidence remained hidden, out of sight to regulators, doctors and patients. Over the next few years, as OxyContin sales and opioid-related deaths climbed, more than a dozen other judges overseeing similar lawsuits against Purdue took the same tack, keeping the company’s records secret." Read the whole thing here: https://www.reuters.com/investigates/special-report/usa-courts-secrecy-judges/  A reporter for Kiplinger wrote a good article on arbitration and avoiding it in July 2019 -- available online:

https://www.kiplinger.com/article/credit/T016-C000-S002-how-to-opt-out-of-forced-arbitration.html Remember, you have to act fast (by early August) and send Chase a regular, signed, snail-mail letter to keep them from forcing you out of court and into forced arbitration on many of their credit cards: From the Kiplinger story: Write a clear statement rejecting the arbitration agreement, and request a letter of acknowledgment from Chase. Include your name, account number, address and signature, too. Send the letter by certified mail (so that you can prove Chase received it) to P.O. Box 15298, Wilmington, DE 19850-5298. Customers who open a Chase card after the deadline can decline the arbitration clause, too. Good TV news story on "mortgage phishing" -- getting buyers to wire money to the scammers instead of to the sellers.

https://www.kezi.com/content/news/Phishing-scam-targeting-homebuyers-in-Oregon-and-beyond-511906211.html  Tell CFPB: Protect Consumers, Not Abusive Debt Collectors The Consumer Financial Protection Bureau’s proposed debt collection rule (Docket CFPB-2019-0022) would let debt collectors text you or email you without permission, and let them contact you up to 7 times per week, per debt, and would also let them file suits over debts without confirming the debtor’s identity or amount owed. The CFPB is accepting public comments on the new rule until August 19. Please take action today - Submit your comments on Docket No. CFPB-2019-0022, and spread the word! Encourage others in your network to help preserve strong consumer protections! Click the "Download File" link just below to see what's wrong with the proposed rule and the changes needed!

There are no “quick fixes” to clean up your credit  The Braille and Talking Book Program

offers Veterans who have difficulty with regular print materials the return of the gift of reading. The Joy and Freedom of Reading Whether escaping into a great novel or staying current with popular magazines, the freedom and independence of reading are only a few steps away. This program, from the National Library Service (NLS) and the Library of Congress, provides talking books, audio magazines, and digital talking-book players free of charge. Any honorably discharged Veteran who is * blind * has low vision, or * a disability preventing the reading of traditional materials is eligible. Participants choose whether their selected reading materials are delivered by mail, downloaded from the web-based service BARD (Braille and Audio Reading Download) or through the BARD mobile app for smartphones and tablets. NLS maintains a vast catalog of titles and publications from the latest best-sellers to timeless classics. Plus, Veterans have preferential status in the lending of materials and equipment. The Braille and Talking Books Program is accomplished through a nationwide network of libraries to serve citizens and Veterans living inside the U.S. or abroad. Applying for this service is easy. Call the National Library Service at 1-888-NLS-READ (1-888-657-7323) or visit them on the web at www.loc.gov/ThatAllMayRead Veterans served to protect freedom. Now let National Library Service provide the freedom for all to read. Mortgage Closing Scams: How to protect yourself and your closing funds By Melissa Yu – JUN 03, 2019 Your Mortgage Closing Checklist Closing is one of the most important stages of buying a house. Learn how to prepare and what to expect so you can close with confidence. Closing on a new home can be one of your most memorable life moments. It’s the final and one of the most critical stages in the home-buying journey, but with the exchange of key paperwork and a sizable down payment, it can also be a stressful experience, especially for first-time homebuyers. The FBI has reported that scammers are increasingly taking advantage of homebuyers during the closing process. Through a sophisticated phishing scam, they attempt to divert your closing costs and down payment into a fraudulent account by confirming or suggesting last-minute changes to your wiring instructions. In fact, reports of these attempts have risen 1,100 percent between 2015 and 2017, and in 2017 alone, there was an estimated loss of nearly $1 billion in real estate transaction costs. While it’s easy to think you may not fall for this kind of scam, these schemes are complex and often appear as legitimate conversations with your real estate or settlement agent. The ultimate cost to victims could be the loss of their life savings. Here’s what you should know and how to avoid it happening to you. How it works Scammers are increasingly targeting real estate professionals, seeking to comprise their email in order to monitor email correspondences with clients and identify upcoming real estate transactions. During the closing process, scammers send spoofed emails to homebuyers – posing as the real estate agent, settlement agent, legal representative or another trusted individuals – with false instructions for wiring closing funds. How to avoid a mortgage phishing scam

What to do if it happens to you

While it can be easy to think you’ll never fall for a scam of this nature, the reality is that it’s becoming more and more common, and the results can be disastrous for eager homeowners. By being mindful and taking a few important steps ahead of your closing, you can protect yourself and your loved ones. To learn more about the closing process, including how to prepare for your closing and common pitfalls to avoid, check out our Mortgage Closing Checklist. For information and resources for the each stage of the home-buying journey, visit the Bureau’s Buying a House tool. The resources on mortgage closing scams are part of the Consumer Financial Protection Bureau’s work to protect consumers from unfair, deceptive, or abusive practices. We arm people with the information, steps, and tools that they need to make smart financial decisions.

Mark Twain once said that Congress was America's only native criminal class. But that's because Twain didn't live to see today's national banking chains and financial institutions, which all make Congress look like a choir of saints. The case below is yet another example of why you should NEVER accept "paperless billing" when dealing with a big bank or other institution, ESPECIALLY ON YOUR MORTGAGE, which is likely the biggest investment you have. Without a paper bill that you can scrutinize at your leisure and show to other people, it's very unlikely that this scam would have been spotted. The original case<https://f.datasrvr.com/fr1/219/92022/ocwen_first.pdf>  Secretary of State

Corporation Division 255 Capitol St. NE, Suite 151 Salem OR 97310 sos.oregon.gov/Business Contact: Corporation.Division@oregon.gov | 503-986-2200 Public Service Notice Don’t be misled into wasting your hard-earned money! Solicitation can easily be mistaken for official correspondence from the State of Oregon. Your business is not currently due for renewal but will be in about 10 to 12 weeks. The annual report fee for Oregon LLC is only $100. Oregon Secretary of State Corporation Division wants to inform you about a questionable solicitation entitled “2019 – Annual Report Instruction Form." Sent by Workplace Compliance Services – a private, for-profit, out-of-state company – the solicitation offers to file your Annual Report for an extra $85 “processing fee,” which is not required under Oregon law. Official Annual Report notices or forms from the Secretary of State will always include the following: 1. The State of Oregon official state seal. 2. The Corporation Division address, 255 Capitol St. NE, Suite 151, Salem, OR 97310. 3. The Corporation Division phone number, 503-986-2200. Additionally, the outer envelope will specify the mailing is from the “Secretary of State – Corporation Division.” If you’d like to know when your Annual Report is due to be filed with the Secretary of State, visit sos.oregon.gov/bizsearch. We send a reminder via postal mail approximately 50 days before an Annual Report is due. The easiest way to file an annual report or to renew a business is through our online services at sos.oregon.gov/renew. If you’re uncertain whether a solicitation is legitimate, call the Secretary of State Corporation Division at 503-986-2200 or check our Alert web page. Regards, Oregon Secretary of State Corporation Division  Certain kinds of goods -- such as appliances, cars, RVs, motorcycles, vacuums, etc. etc. -- tend to be problems. They are hard for consumers to evaluate objectively, and are often sold with high-pressure tactics by unscrupulous dealers who have a lot of experience confusing the buyers and preventing the buyers from getting help in evaluating the worth of the goods on offer. One of the tricks shady dealers (call them D's) of these kinds of goods use is "selling the paper" immediately after the dealer makes the financed sale (immediately as in "before the ink dries"). By selling the paper, the dealer gets paid immediately and the supposedly innocent lender (call this lender L) acts as if all the shady techniques the seller used are irrelevant to the buyer's obligation to pay on the contract -- even for goods that were totally not as represented and that fell apart as soon as you got them home. Over the years, many consumers have been duped into thinking that even though the dealer ripped them off horribly, they're still stuck on the loan, because the Lender L didn't participate in the fraudulent sale. Because of this ancient game by shady dealers and shady lenders, something called the "Holder Rule" emerged. That name comes from a key phrase in consumer law: "The holder (of the loan) takes the loan subject to all the claims and defenses the buyer would have been able to bring against the seller." But if that's too much legalese, you can simply think of the Holder Rule as the "Keeping the Holder of Your Loan from Weaseling Off the Hook When You Got Scammed Rule." Under this special rule, when you find out you got scammed on goods you borrowed money to buy, you can usually raise the same claims against the Lender (L) that you could have brought against the Dealer (D) -- even though, in theory, Lender L was (supposedly) totally not involved in the shady sale of the goods and didn't make the misrepresentations about the goods. (I say Lender L was supposedly not involved because shady dealers usually or sometimes only send customers who need loans to buy their goods to certain preferred finance companies. Sometimes the lenders even pay kickbacks or "referral fees" to the dealers or the same person owns both. Such "preferred" lenders are well aware of how often the dealer's shoddy goods fall apart or are total rip-offs, but the lender likes to pretend to be completely innocent about what a ripoff the dealer is; these lenders turn a blind eye and pretend that the shady dealer is a reputable seller, and they certainly aren't going to tell you about the holder rule, which lets you bring up the sins of the dealer when you are explaining why you stopped paying the Lender.) FTC Completes Review of Holder Rule |

AuthorJohn Gear Law Office - Categories

All

Archives

December 2022

|

||||||||

|

Lawyerly Fine Print:

John Gear Law Office LLC and Salem Consumer Law. John Gear Law Office is in Suite 208B of the Security Building in downtown Salem at 161 High St. SE. That is right across High Street from the Elsinore Theater, a half-block south of Marion County Courthouse.

John Gear is only licensed to practice law in Oregon. This site may be considered advertising under Oregon State Bar rules. There is no legal advice on this site so do not take anything you read here as advice for your particular problem or situation. And I do not represent you and I am not your attorney unless you have hired me with a representation agreement. While I do want you to consider me when you seek an attorney, you should not hire any attorney based on brochures, websites, advertising, or other promotional materials. All original content on this site is Copyright John Gear, 2010-2022. |

RSS Feed

RSS Feed